Alibaba's March Quarter 2023 Earnings Review

Part 1: Stagnant Revenue Growth, Improving Profitability, and Capital Allocation Updates

Listen:

Hello fellow Investors!

Welcome back to the JB Global Capital Newsletter. A major thank you to all of the new members of our community who joined recently. We are happy to have you.

Special Announcement:

We have recently added the option to pledge to our newsletter. This allows readers to show their support for our work and gives us positive feedback that you find our analysis valuable. If you have been enjoying our content thus far, we highly recommend you consider pledging to the newsletter. If we decide at any point to turn on subscriptions, you will be informed well ahead of time.

Thank you as always for your support!

Business Overview:

Alibaba Group is a big-data conglomerate that owns two of the most popular online shopping sites in China (Taobao and Tmall) and is the world’s largest e-commerce business by gross merchandise value of $1.3T. (Yes. That’s a T as in Trillion). In addition to their retail business, the company owns multiple divisions that facilitate different aspects of commerce such as payments, logistics, digital media, and cloud computing. Since going public in 2014, the company has expanded their services throughout Southeast Asia, Europe, and the Middle East.

More recently, the company has announced that it will be splitting the business into six independent units, each with the ability to raise capital through external financing, setting the stage for IPOs and spin-offs. The six business units include:

🏭 China Commerce

🚚 Cainiao Smart Logistics

☁️ Cloud Intelligence

🛒 Local Consumer Services

🌏 International Commerce

🎥 Digital Media and Entertainment

March 2023 Financial Highlights - Figures converted to USD 0.00%↑

Revenue: $30.32B (+2% y/y)

Adj. EBITDA: $3.64B (+60% y/y)

Adj. EBITDA Margin: 12.0%

Free Cash Flow: $4.70B

Free Cash Flow Margin: 15.6%

Alibaba recently reported financial results for the quarter and fiscal year ended March 31, 2023. Revenues for the quarter were $30.32B, a slight miss on analysts’ expectations and a mere +2% growth year-on-year. During the earnings call, management attributed this low revenue growth to weaker-than-expected consumption spending in China, and intense market competition from rivals.

“In the past few months, we have noticed a gradual recovery in China consumption, but consumer confidence and spending power still need further momentum. At the same time, competition among the multiple consumption platforms is still fierce, and everyone is trying to capture the incremental demand with more value-for-money products and services.” – Daniel Zhang, CEO

While Zhang did not name the competitors directly, it is safe to assume that he is largely referring to the e-commerce businesses, Pinduoduo, JD, and ByteDance.

Revenues from the cloud computing segment were especially disappointing, declining y/y by -2%. Management attributed the decrease in cloud revenue to a weak macro backdrop, and from a top customer phasing out Alibaba's cloud services due to data security regulations for their international business. While we are disappointed with the Cloud segment results to date, we are encouraged by three key data points, which we believe still hold true:

Alibaba Cloud is the largest player by market share in China and fourth largest in the world. We believe that Alibaba will remain as a market leader due to key competitive advantages stemming from capital intensity requirements and technological capabilities.

China’s Cloud market is expected to grow to $90B by 2025 as per McKinsey Research. As the market leader, we expect Alibaba to reap the benefits with the growth in Cloud adoption in both Mainland China, and Southeast Asia.

Digital transformation trends are expected to grow over the long-term due to improved economics for businesses in every industry. Some of the digital transformation trends include wider adoption of low code platforms, increased migration to the cloud, greater leveraging of AI technologies, and increased automation. Cloud providers like Alibaba stand to benefit greatly from these trends, as they exponentially increase the demand for data storage and capabilities.

While revenue growth struggled to impress analysts and investors alike, bottom-line earnings for the quarter improved significantly to $3.64B, a 60% year-on-year growth rate. The material improvement in earnings was attributed to successful cost-cutting measures and improved profitability in their non-core segments, such as local consumer services and smart logistics. We are impressed by the company’s overall profitability as Alibaba continues to produce significant amounts of free cash flow. In the fiscal year ended March 31 2023, Alibaba generated $25B in free cash flow ($20B after deducting SBC). To put this figure into perspective,

Alibaba generated double the amount of FCF than their two largest competitors combined; (Pinduoduo with $6.94B, and JD with $6.03B).

Share Repurchases and Capital Allocation Update

On another positive note, Alibaba repurchased $10.8B of shares for the Fiscal Year ended March 31st, 2023, the largest yearly buyback completed in the company’s history. While we are encouraged to see the company buying back stock, we believe that they could be more aggressive in this area, given their strong cash position and low valuation. Alibaba’s CFO, Toby Xu, addressed the company’s capital allocation plans by announcing the formation of the Capital Management Committee. This Committee was created to undertake capital allocation decisions to improve shareholder return through buybacks and spin-offs. Speaking directly to these goals, Alibaba’s CFO stated,

First, the strength of our balance sheet and our cash position is a competitive advantage in an uncertain environment. While we maintain a prudent approach to our capital structure, we will be focused on improving the return on invested capital in managing the assets of the company.

Second, we will design, review, and implement EPS accretive activities including consistent share buybacks to reduce our outstanding share count, while maintaining discipline in managing our ESOP programs.

Third, we will explore all options to enhance shareholders’ return by achieving more transparency in the value of our assets and returning capital to shareholders, including subsidiary fundraising, IPOs and spin-offs.”

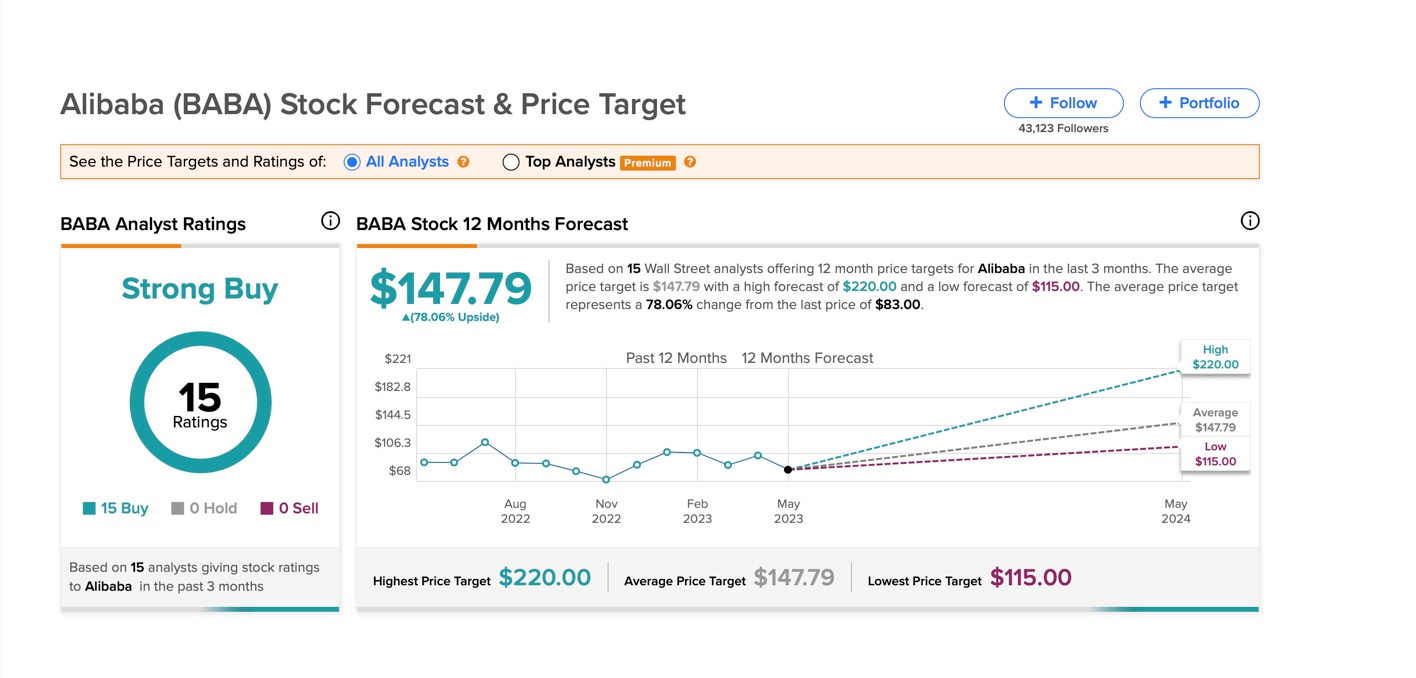

Since the earnings were announced, Alibaba’s stock has declined by ~12%, underperforming the general market. Much of the recent sell-off has been attributed to a weaker-than-expected recovery in China, increasing competition, a rise in geopolitical tensions, and the strengthening of the U.S. dollar in relation to the Chinese Yuan. Analysts covering the stock however remain bullish on the shares, with 15 Buy recommendations and 0 Sell Recommendations, with an average price target of $147.79. This would indicate a significant discount to intrinsic value, as Alibaba currently trades in the low $80s at the time of writing.

This concludes Part 1 of our earnings review for Alibaba. In Part 2, we will delve deeper into the planned spin-offs and provide updated valuation models for Alibaba’s shares. We hope you have enjoyed our analysis thus far. As a reminder, we have added the option to pledge a future subscription for our newsletter. If you enjoy our content, consider pledging and share with a friend. Your support is greatly appreciated.

Until next time!

Sincerely,

Jack Beiro, MBA

JB Global Capital

BABA 0.00%↑ JD 0.00%↑ PDD 0.00%↑

The information contained herein represents the author’s opinion and is for informational purposes only. Nothing in this newsletter should be construed as legal, tax, investment, or financial advice. No opinion expressed by the author should be construed as a specific inducement to make a particular investment or follow a particular strategy. The author may hold positions in securities mentioned in the newsletter and may buy or sell securities at any time. The author may express opinions based on information he considers reliable, but no guarantee or warranty is made with respect to such information’s completeness or accuracy, and the author is under no obligation to update or correct any information provided. Please consult your own financial or investment advisor before acting on any information provided herein.