Amazon.com (AMZN) Q3 2023 Earnings Review

Listen:

Hello fellow investors!

Welcome back to the JB Global Capital newsletter. Today we will be reviewing Amazon’s Q3 financial results. We will also be sharing our three valuation models for Amazon which include NAV, EPV, and a DCF model. We hope you enjoy the article!

Business Overview:

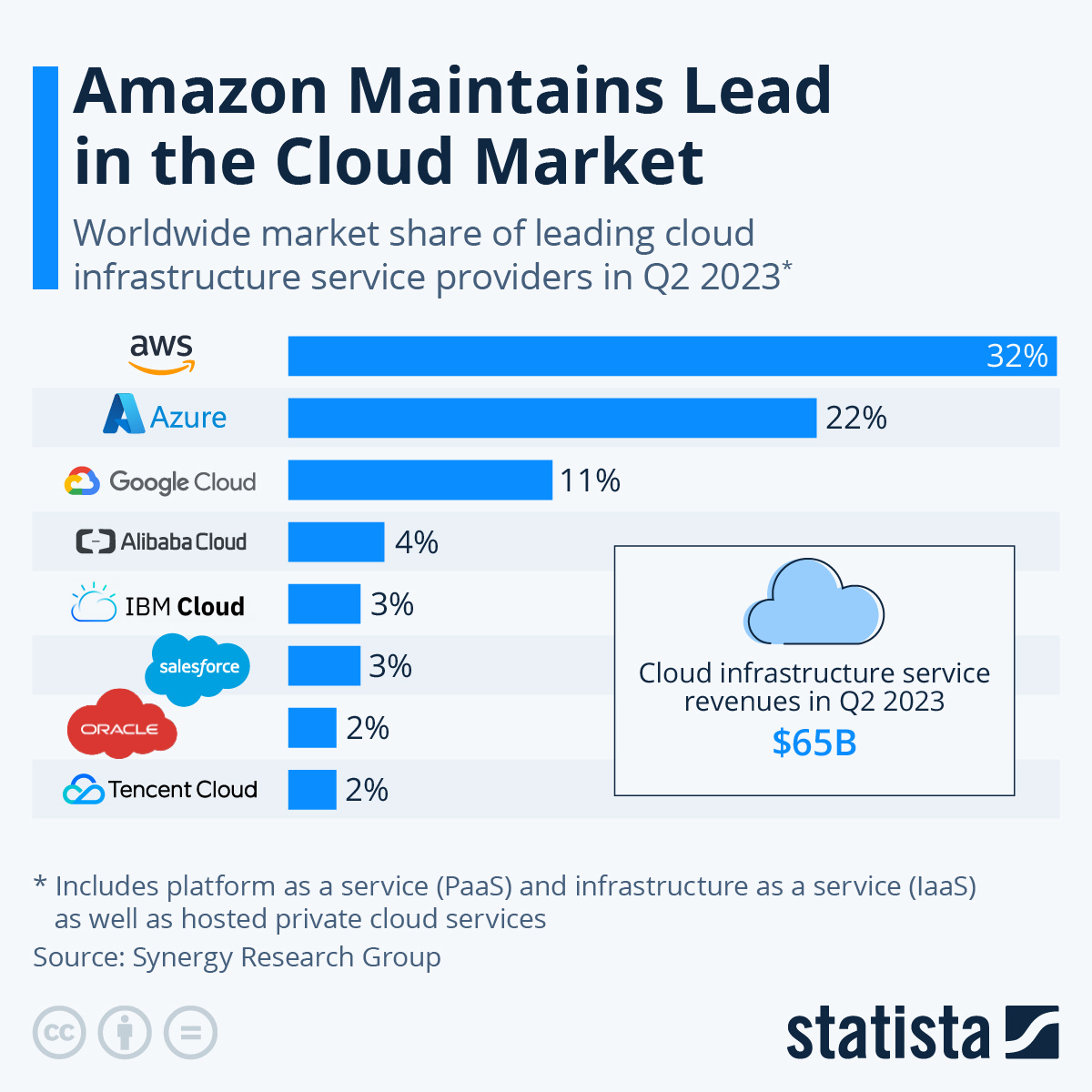

Amazon dominates its served markets, notably e-commerce and cloud services. The company has become ubiquitous in modern culture to the point that if you are reading this, there is a very high probability that you use one of its products or services habitually. Amazon benefits from numerous competitive advantages and has emerged as the clear e-commerce leader thanks to its size and scale, which yields an unmatched selection of low-priced goods for consumers. The secular drift toward e-commerce and digitization continues unabated with the company continuing to grind out market share gains despite its size. Amazon’s supplemental offerings including Prime Video, Kindle, and Amazon Pharmacy bolster the ecosystem by helping attract new customers while strengthening the value proposition for existing customers.

Q3 Financial Highlights:

Revenue: $143.1B (+13% y/y)

Operating Income: $11.2B (3.5X y/y)

Operating Income Margin: 8%

Free Cash Flow: $8.7B

Free Cash Flow Margin: 6%

Amazon reported excellent third-quarter results and provided better-than-expected guidance for the fourth quarter. Third-quarter revenue grew 13% year over year as reported and 11% in constant currency, to $143.1 billion. The two key segments, AWS and advertising, grew 12% and 26% as reported, respectively, over the year period. Amazon’s advertising growth continues to outpace that of its large internet peers. Profitability came in strong with free cash flow of $8.7B, which equates to a 6% margin. Based on management’s guidance and statements on the earnings call, the business is expected to remain healthy in the near term with resilient consumer spending and AWS contracts accelerating into the end of the quarter.

Amazon’s impressive results are founded in some basic but essential corporate priorities such as obsessing over the customer experience, lowering the cost to serve, and investing for future growth. The company has thus far made tremendous progress on each of these goals through continued operational efficiency and a future focused capital allocation strategy. During the earnings call, CEO Andy Jassy emphasized a bullish view on the future of cloud computing services and generative A.I. applications.

“As you can tell, we're focused on doing what we've always done for customers, taking technology that can transform customer experiences and businesses, and democratizing it for customers of all sizes and technical abilities. We're innovating and delivering at a rapid rate and our approach is resonating with customers. The number of companies building generative A.I. apps in AWS is substantial and growing very quickly. Every one of our businesses is building generative AI applications to change what's possible for customers, and we have a lot more to come.” - Andy Jassy, Q3 Earnings Call

Ultimately, we view generative A.I. as an absolute game-changer for Amazon in the areas of predictive demand forecasting, inventory management, and personalized content. Based on managements performance thus far, we see no reason that the company will not succeed in growing profits materially in the years to come. The company maintains well positioned to capture the secular trend of digital transformation occurring in various aspects of commerce. While we expect competition to increase in the years ahead, we view the barriers to entry high and Amazon’s lead wide enough to remain the dominant Cloud player for the foreseeable future.

Valuation:

Amazon’s Net Asset Valuation = $90B or $8.76 per share. We use this net asset value as a floor liquidation value for the business, and to analyze the strength of the company’s balance sheet. As some accounting values are more reliable than others, we accept or adjust the stated numbers on the financial statements. This process leads to an ultra-conservative estimate of Amazon’s stated net-asset value.

Amazon’s EPV Valuation= $454B or $44.17 per share. Earnings Power Value is a technique for valuing stocks by assuming the sustainability of current earnings and cost of capital, but assuming no future growth. We use EPV as a conservative valuation method for analyzing what a business is worth in its current state. While it is unrealistic to believe that Amazon’s profits will remain stagnant going into the future, we use the below figures as a yardstick to measure the viability of an investment at current earnings.

Amazon’s DCF Valuation= $1.16T or $112.76 per share. This valuation assumes decelerating revenue growth over the next 10 years and a WACC of 9.40%. At the time of writing, Amazon is currently valued at $127.77 per share. This would indicate that Amazon is trading slightly above our estimate of fair value. While Amazon is undeniably one of the greatest businesses of our generation, the market is currently pricing in much of the impressive qualities that we have highlighted in our analysis.

We hope you enjoyed the write-up. If you did, make sure to leave a like and share with a friend.

Until next time,

Jack Beiro, MBA

JB Global Capital

The information contained herein represents the author’s opinion and is for informational purposes only. Nothing in this newsletter should be construed as legal, tax, investment, or financial advice. No opinion expressed by the author should be construed as a specific inducement to make a particular investment or follow a particular strategy. The author may hold positions in securities mentioned in the newsletter and may buy or sell securities at any time. The author may express opinions based on information he considers reliable, but no guarantee or warranty is made with respect to such information’s completeness or accuracy, and the author is under no obligation to update or correct any information provided. Please consult your own financial or investment advisor before acting on any information provided herein.