Investment Case: Expedia Group

[Guest Post] By Simone Portaro

Audio Version:

Greetings Fellow Investors!

In today’s special edition of the newsletter, we would like to introduce a guest writer, Simone Portaro. Simone is a Ph.D. student in Applied Mathematics with a great passion for value investing and business analysis. Today’s investment case is on Expedia Group [ EXPE 0.00%↑ ]. We hope you enjoy the article!

Click here for Simone Portaro’s Linkedin Profile

Business Overview:

Expedia Group (EXPE) is a dominant player in the online travel agency (OTA) industry, ranking as the world's second largest OTA in terms of bookings. The company offers a multitude of services, with lodging accounting for 76% of its total sales in 2022. Other revenue streams include rental cars, cruises experiences, and other travel-related services (14%), advertising revenue (7%) as well as air tickets (3%).

Expedia has built a leading network of online travel services, which has driven a strong user base that has remained resilient and consistently grown over multiple years, surpassing various economic cycles. The sustained growth and stability of Expedia's user base serve as a proof of the high quality and reliability of its business operations.

Expedia Group owns a diversified portfolio of well-known brands such as Expedia.com, Hotels.com, Vrbo, Orbitz, and several other minor brands. In addition to its core OTA operations, Expedia has ventured into the travel media sector through the acquisition of Trivago (TRVG). The company currently holds a 61.6% stake in Trivago, with the aim of further expanding its reach and influence within the industry. Expedia traces its origins back to 1996 when it was initially established as a division of Microsoft. Over the course of nearly three decades, it has consistently broadened its scope of operations while maintaining its position as a market leader.

Why we like the business:

Expedia Group holds a dominant position in the U.S. market, while its international presence is comparatively weaker. However, this presents an opportunity for future growth in high-margin regions such as Europe and emerging markets like Southeast Asia and Latin America.

During the Q1 2023 earnings call, Peter Kern, CEO of Expedia, stated,

“There are big pockets of (customers) that we don't touch right now that are opportunities, and there are also pockets of them that we used to touch less efficiently that we think we can go back to with strength.

So I think it's not going to be a huge story in the numbers this year, although we have seen a great comeback in EMEA, in Asia, in Latin America, where we do participate. But that's a bigger story over time as we get our One Key launch done, as we get our product complete and as we can start to move our strategy more holistically into new markets and target the right customers for us.”

It's important to note that the competition in Southeast Asia from platforms like Agoda.com and Trip.com is intense, so the company cannot rely solely on these markets for significant growth.

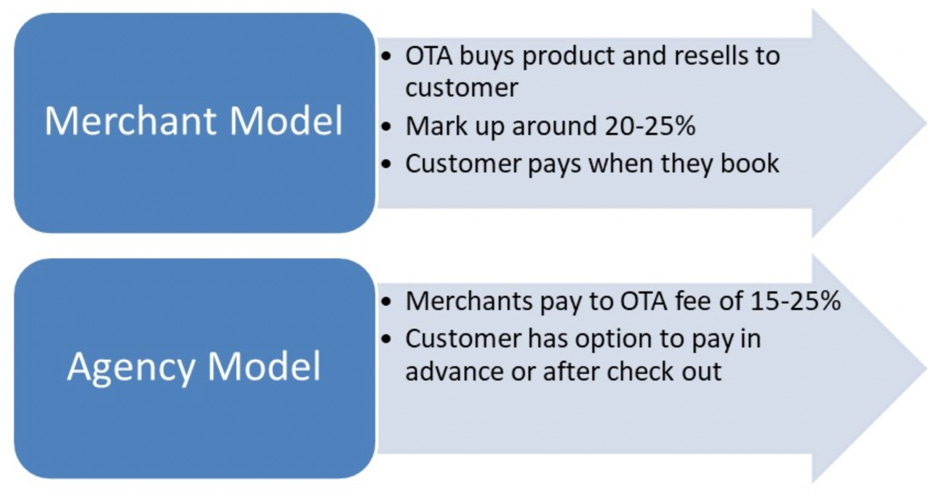

The main sources of revenue for Expedia are derived from the merchant and agency models.

Merchant model: Under the merchant model, Expedia acts as the intermediary for booking hotel rooms, alternative accommodations, airline seats, car rentals, and destination services from travel suppliers, assuming the role of the merchant of record.

Agency model: Conversely, under the agency model, Expedia forwards reservations made by travelers to the relevant travel suppliers, who serve as the merchant of record.

In return, Expedia earns commissions from both the travel supplier and the traveler. Typically, the commission rates for hotel bookings range from 15% to 25%, while margins for air travel tend to be lower. However, the revenue margin from total gross bookings fluctuates between 10% and 15%, aligning with competitors like Booking.com.

Expedia has established itself as a leader in the Business-to-Business (B2B) sector, forging partnerships with renowned companies such as Mastercard and Sofi. Notably, the B2B segment has witnessed exceptional growth, with a remarkable YoY revenue increase of 54% in Q1 2023. But Expedia is not solely hotels. In November 2015, it acquired Vrbo, an OTA specializing in vacation rentals and alternative accommodations, aiming to challenge Airbnb's dominance in the market. Although some argue that Expedia may have overpaid for Vrbo and other acquisitions, the Vrbo acquisition stands out as a strategic move. It has enabled Expedia to penetrate the growing vacation rentals market and directly compete with Airbnb for market share.

Lastly, starting in July 2023, Expedia Group will introduce the One Key program in the United States, with plans to expand into additional markets in 2024. This program aims to consolidate the loyalty programs of Expedia Group's three major brands: Expedia.com, Hotels.com, and Vrbo. By integrating these loyalty programs, Expedia seeks to enhance customer loyalty and retention.

Expedia Group has successfully established a robust network of properties, contributing to the supply side of the network effect equation. This network effect has led to a significant increase in end-user traffic and bookings, driving strong demand for Expedia's services. As a result, the company has experienced enhanced brand recognition and a flywheel effect, wherein the growth of properties on the platform attracts more customers to make bookings, subsequently attracting even more properties to join the platform. This virtuous cycle strengthens Expedia's position in the market and reinforces its ability to capture a larger share of the travel booking industry. We believe that the OneKey program will contribute to strengthen the network effect.

Considering the success of Booking.com's loyalty program, Genius, we anticipate that Expedia Group can achieve a similar level of customer loyalty and retention by implementing reward programs and offering favorable discounts. While the brand reorganization onto one front-end stack can be confusing at first glance for customers, thus a headwind for the short-term, we believe these initiatives are expected to provide added value to customers, incentivizing repeat bookings and leading to a better ROIC and revenue growth.

If you are enjoying the content, make sure to subscribe for more!

Capital Allocation, Balance Sheet and Management:

Expedia Group’s capital allocation strategy has faced criticism in recent years due to questionable decisions regarding overpriced acquisition and disorganized buybacks. We agree with such critiques. However, there has been a positive change in the company’s Chief Financial Officer (CFO) position, which took place in October 2022. The appointment of Julie P. Whalen, a former CFO of William-Sonoma (WSM) and long-term board member, brings optimism as she has a proven track record of implementing strategic and effective buybacks while efficiently allocating capital expenditure (CapEx) and maintain a modest leverage ratio (2.7x Adjusted EBITDA, projected to be 2-2.1x at the end of 2023). In the first 4 months of 2023 Expedia repurchased 6 millions shares, which represents 3.5% of all the shares outstanding. Overall cash and long-term debt sum up to zero, which gives a clean balance sheet.

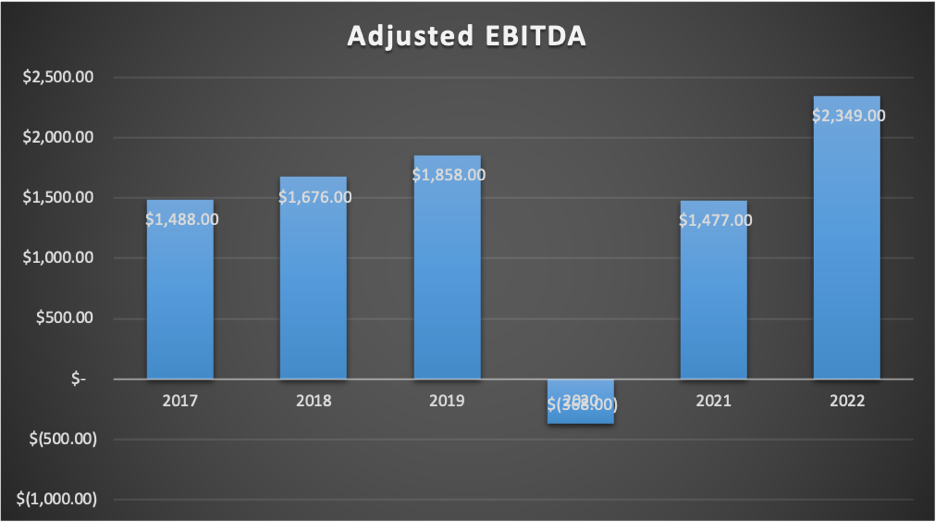

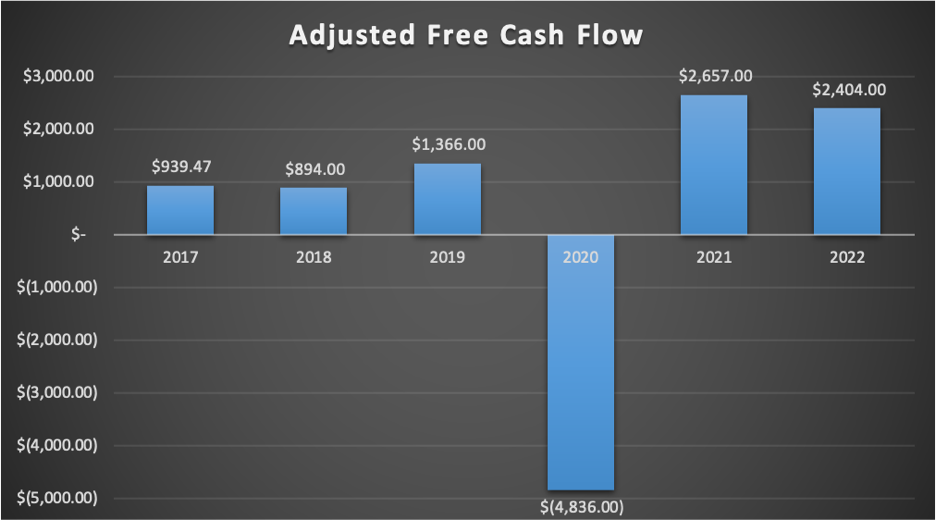

In April 2020, Peter Kern was appointed as CEO of Expedia Group, a challenging period for an online travel agency (OTA) due to the impact of the COVID-19 pandemic. Despite the natural complications caused by the pandemic, the management team successfully steered the company's operations back to pre-pandemic levels, matching or even surpassing the performance of 2019 in terms of EBITDA and Free Cash Flow.

Furthermore, the management team has demonstrated agility and responsiveness to market shifts in the dynamic OTA industry. Notably, Expedia Group was the first OTA to integrate ChatGPT into its iOS app, showcasing their commitment to embracing emerging technologies and enhancing customer experience. This shift towards integrating AI is a key point for Expedia Group. We firmly believe that Expedia stands to gain significant advantages from the rise of AI. By leveraging AI technologies, the company can potentially reduce customer care expenses, which are accounted for in the cost of revenue. This reduction in expenses can lead to an expansion of gross margins while simultaneously providing an enhanced service experience for customers.

Valuation:

Expedia currently has a market capitalization of $16.7 billion. The company's Forward PE ratio stands at 11.9, which is lower compared to the respective ratios of 19.72 for Booking.com and 34.72 for Airbnb. Similarly, Expedia's Price-to-Sales (PS) ratio is 1.48, significantly lower than the ratios of 5.66 for Booking.com and 9.88 for Airbnb. This notable discount relative to its peers may be justified by the company's execution under previous management. However, it also presents an opportunity for potential upside if the current management can improve operational efficiency and drive better capital allocation.

With the current tailwinds favoring remote work and a paradigm shift in vacation preferences exiting the pandemic, the entire sector is expected to witness modest growth in the high single-digit to low teens. We believe Expedia can benefit greatly from these shifts in customer preferences.

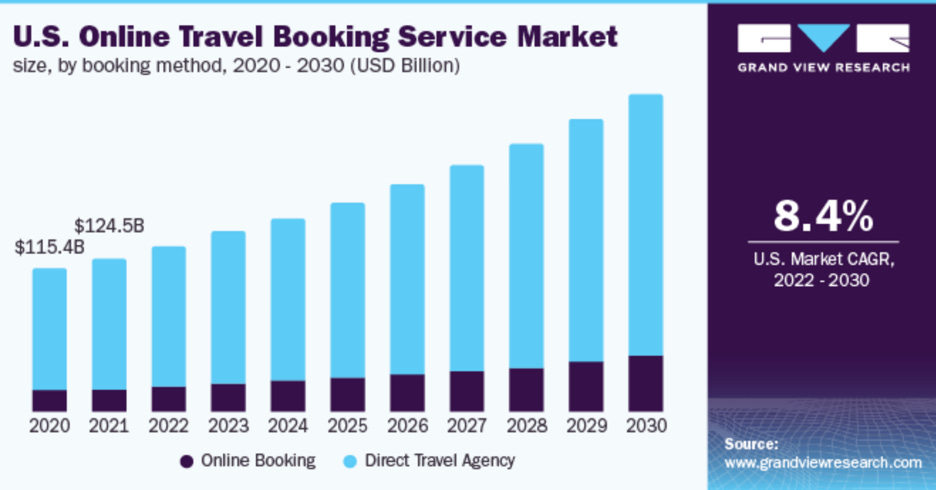

Moreover, in the U.S., where Expedia has the leader position, online booking is expected to grow faster than direct travel agency. This secular trend of increasing preferences for online booking over traditional channels presents a significant opportunity for Expedia Group to capitalize on.

Considering the current favorable trends in the market, such as the increasing popularity of remote work and the changing vacation preferences following the pandemic, the entire travel sector is projected to experience moderate growth ranging from high single digits to low teens.

In this regard, we believe that Expedia Group is well-positioned to capitalize on these opportunities. While management expresses optimism regarding future growth prospects, we have adopted a more conservative approach in our analysis. We have assumed a compounded annual growth rate (CAGR) for the next 10 years in a range from 1% to 8% on Adjusted Free Cash Flow, incorporating adjustments accounting for stock-based compensations as a full expense. Although our approach may be considered conservative, we believe it provides a margin of safety in our valuation. Historically, Expedia's Adjusted Free Cash Flow has grown at a rate of 12%, but the company's capital allocation practices have been questionable. Utilizing a DCF model with a discount rate of 15%, we arrive at the fair value estimate to fall within the range of $120 to $185 per share. Hence, we believe shares are undervalued for a very good compounded return.

Catalysts for Share Price Appreciation:

Optimization of margins

Current low price ratios relative to peers

New management with a strong history of execution and a unified network plan

Increasing buybacks

Growth in the travel industry

Thanks for reading!

Written by Simone Portaro

Edited by Jack Beiro

JB Global Capital

The information contained herein represents the author’s opinion and is for informational purposes only. Nothing in this newsletter should be construed as legal, tax, investment, or financial advice. No opinion expressed by the author should be construed as a specific inducement to make a particular investment or follow a particular strategy. The author may hold positions in securities mentioned in the newsletter and may buy or sell securities at any time. The author may express opinions based on information he considers reliable, but no guarantee or warranty is made with respect to such information’s completeness or accuracy, and the author is under no obligation to update or correct any information provided. Please consult your own financial or investment advisor before acting on any information provided herein.

| A guest post by

|