Q3 2024 Investor Letter

A Reflexive Shift in the China Narrative

October 2, 2024

To our Partners:

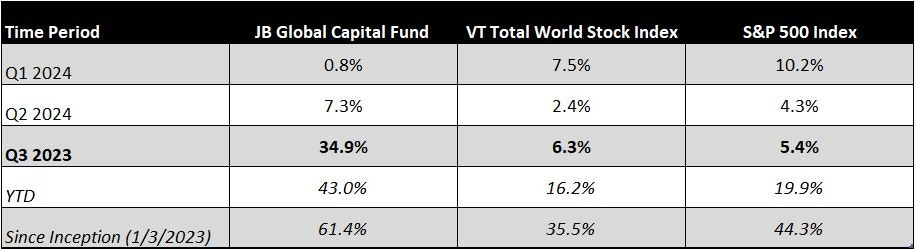

Q3 was a good quarter. It was not a good quarter because we had a gain of ~35%, but because our performance was substantially better than our benchmarks; the S&P 500, and the VT Total World Stock Index. As a restatement, our goal is to outperform relative to the indexes over a period of 3-5 years. While absolute gains in the fund are pleasant to announce, our goal would be equally realized if our fund lost 5% for the quarter and the indexes lost 10%. We find it unreasonable to aim for consistent positive market returns as financial markets are inherently cyclical. We instead aim for finding well managed businesses with competitive advantages in growing industries selling at a discount to a conservative estimate of fair value.

Results and Reflections

Our results to this point have been promising. While it is still early days, we have outperformed the benchmarks by a significant factor since the inception of the fund.

The quarter’s results can be attributed to a few major developments that unfolded over the previous month. The first is the federal reserve’s decision to begin lowering interest rates in the United States; a larger than expected cut in September signaled the start of a new cutting cycle alongside slowing inflation. (i.e. a soft landing). Our U.S. equities increased in value due to the increased liquidity and anticipated economic activity that comes with lower interest rates. This decision also had far reaching consequences as it allowed the Chinese government to lower their interest rates, (without currency depreciation) and begin expansive monetary and fiscal reforms to combat the current economic crises. During the quarter, China’s yuan surged to a 16-month peak on the back of optimism related to the proposed rescue package.

The surge in Chinese equities over the quarter has caught the attention of many prominent investors including David Tepper, Michael Burry, and Rob Vinall of RV Capital. In discussing Chinese equities in his latest investor letter, Vinall wrote the following:

“The valuations in China are the most astonishing I have seen in my investment career, including during the Great Financial Crisis of 2008/09. Take the companies we own. They are blue chips with dominant competitive positions in their respective industries. They are highly profitable. They have oodles of net cash. They are growing at the top and bottom line despite the struggling Chinese economy. Despite these favorable characteristics, they trade at P/Es ranging from mid-single digits to low double digits, and […] are aggressively returning cash to shareholders.”

We believe that we are at the beginning of a reflexive shift in narrative for Chinese equities. The shift in narrative that we are witnessing has the potential to start the next bull market, provided that the monetary and fiscal policies take effect and kickstart economic activity. Caveat: The wild card of investing in China is always a political one. The deteriorating relationship between the U.S. and China has been one of the narrative drivers that have kept Chinese equities under owned and under appreciated by global investment funds. In the next section, we will discuss our views on the upcoming U.S. election and the role it plays (if any) in our investment decisions.

The Laws of Economics vs. Political Reality

“The wonder of markets is that they reconcile the choices of myriad individuals.” – William Easterly

As the U.S. election is just months ahead, we find it appropriate to disclose our thoughts here on investing through political reality. In the run up to the election, both candidates have been making economic policy promises that seemingly ignore economic reality or at least oversimplify it to a nonsensical degree. Trump’s call for a 60% tariff on all Chinese goods and Harris’s attack on grocery profiteering are merely two examples of proposals that have significant economic costs that the candidate seemingly ignores. Politicians can promise whatever they want regarding the economy, but they won’t be able to deliver if their promises fly in the face of economic reality. Ultimately, the laws of economics are irrefutable.

In other words, governments can pass laws designed to compel or discourage behavior, but in general they can’t mandate economic outcomes due to the complexity of second-order consequences and the ever-changing nature of causes and effects. Many command economies of the past have failed due to this fundamental misunderstanding. The incentives provided by free markets efficiently direct capital and other resources where they’ll be most productive. They prompt producers to make the goods people want most and workers take the jobs where they’ll be most productive. In general, capitalism produces the highest standard of living for society because it allows the system to balance its shortages and excesses through natural processes of the free market.

As a way of illustrating the discrepancy between economic systems in history, we can look at what happened to Korea after WWII. Eighty years ago, Korea was a single country. Following WWII, it was split into two countries, South Korea (under U.S. influence) and North Korea (under Soviet influence). Both countries at the time of the split consisted of similar people, culture, geography, and resources. According to the CIA’s Worldbook, North Korea’s GDP per capita is most recently estimated at $2,000 per person versus $50,000 in South Korea. There are political differences in addition to economic ones, but we think it’s fair to say that much of this discrepancy in economic outcome can be attributed to free market capitalism.

At this point, a reader might ask, “What about China? Their GDP has grown at nearly 9% per annum for the last 45 years, and in 2010, became the world’s second-largest economy. How could that be?” China is often misunderstood in the western world due to the contradiction between a communist political ideology, alongside a market lead capitalistic economy. We, in the western world, predominately think of China as a “communist country,” with state-owned enterprises, industrial policy, and an autocratic leader. However, if you study the economic policies over the last 45 years, you will see a pragmatic adoption of the incentives provided by capitalism such as efficiency gains, free capital flows and ultimately, the reduction of poverty on a grand scale.

As far as our portfolio is concerned, we do not consider political outcomes when making individual investment decisions. We aim to be informed about political headwinds or tailwinds as it relates to business sentiment and the general stock market, but do not make decisions by forecasting economic policies and their effects on our specific businesses. We believe that decisions regarding long-term investments should be based in economic reality rather than the political party that happens to be in power at the time of the decision. Over a long-term holding period, our businesses will see a variety of challenges and opportunities related to changes in the political landscape. However, if the investment is based in economic reality, we believe there is a high chance of success, regardless of which political party is in power at any given time.

Portfolio Company Update:

Alibaba Group Holdings BABA 0.00%↑

During the quarter, Alibaba reported earnings that were mixed. Consolidated revenue grew mid-single digits while free cash flow decreased 56% compared to the same quarter last year. The decrease in cash flow was due to higher expenditure related to Alibaba Cloud and increased promotional spending in their Taobao and Tmall Group. The company has continued to repurchase shares at attractive levels. In the June quarter alone, Alibaba reduced their total shares outstanding by 2.3%, net of any share-based compensation.

During the earnings call, CEO Eddie Wu took questions regarding the higher CapEx spend related to A.I. Wu defended the increased spend, stating,

“If you look at the pipeline, you know there's going to be ongoing demand. So, whether it's for training or inference or API calls, what we see when we're making this kind of capex investments, as soon as we get a server up, a server is instantly running at full capacity. There's that kind of demand. So, we can expect to see a very high ROI over these next quarters because we're building compute power to meet existing demand and that new compute power coming online is getting instantly taken up and running at full capacity on day one.”

The company has continued to make strides in artificial intelligence, releasing more than 100 open-source A.I. models and boosting the capabilities of its proprietary technology. During the quarter, the number of paying users using Alibaba Cloud’s AI platform increased by over 200% Q/Q. Alibaba also launched a new text-to-video tool based on its AI models. This allows users to input a prompt, and the AI will create a video based on it, similar to OpenAI’s Sora.

On September 20th, 2024, Alibaba announced a new collaboration initiative with Nvidia (NVDA 0.00%↑) that will enable Chinese automakers to advance the autonomous driving experience for smart vehicle owners. The collaboration brings together China’s largest cloud computing platform with the globe’s largest semiconductor powerhouse. While the earnings impact from this collaboration could be negligible, we find this announcement to be indicative of the lead that Alibaba has in A.I. compared to its peers. Nvidia, being the largest and most powerful player in the A.I. space, is not constrained in who they can collaborate with. The fact that they chose Alibaba to collaborate with (rather than Baidu or Tencent), is very telling of the competitive strength of Alibaba’s LLM, Qwen 2.5.

There are a few things that are becoming apparent as the A.I. wave continues to strengthen around the globe:

Alibaba is emerging as the top A.I. player in Asia (followed by Baidu and Tencent)

Alibaba is currently the largest Cloud Computing player in Asia

Demand for Cloud services and A.I. are interconnected and growing exponentially. Alibaba can benefit by providing both services to a massive user base. (1 billion + globally)

The use cases for A.I. applications are seemingly endless.

We believe that over the next 5 years, these trends will naturally continue to the benefit of the companies that have been willing to invest at this crucial stage of development. While most of the value in Alibaba’s business today is in global e-commerce, we are looking forward to the full integration of A.I. with e-commerce and all of the optionality that brings with it.

The Portfolio

Since inception, we have made 16 investments in 7 industries as classified by Morningstar. While the investments span throughout various sectors, there is material concentration in the sectors of internet retail, financial services, and cloud computing. We anticipate high volatility in the fund due to portfolio concentration, emerging market risk (largely in China), and a contrarian investment strategy. We would like to thank our partners and readers for their continued support.

Until the next quarter,

Jack Beiro, MBA

JB Global Capital

The information contained herein represents the author’s opinion and is for informational purposes only. Nothing in this newsletter should be construed as legal, tax, investment, or financial advice. No opinion expressed by the author should be construed as a specific inducement to make a particular investment or follow a particular strategy. The author may hold positions in securities mentioned in the newsletter and may buy or sell securities at any time. The author may express opinions based on information he considers reliable, but no guarantee or warranty is made with respect to such information’s completeness or accuracy, and the author is under no obligation to update or correct any information provided. Please consult your own financial or investment advisor before acting on any information provided herein.