Selling StoneCo Ltd. (STNE)

Why We Sold Our Position in StoneCo

As of May 9th, 2024, we have sold our entire position in the Brazilian merchant acquirer business StoneCo STNE 0.00%↑ , for a net return after tax considerations of 61.4%. This sale provides us with an opportunity to discuss our thinking when it comes to selling a portfolio company and analyze the facts and reasoning behind our decision. As always, thank you for subscribing to JB Global Capital. We hope our discussions are valuable to you in your own investing journey. Let’s get to work!

Disclaimer: The following is not financial advice. The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice.

We published our original investment thesis for StoneCo on March 18th, 2023. In the write-up, we discussed the business overview, qualitative and quantitative factors affecting the business, and our thoughts on the investment opportunity. Our thesis was backed by three fundamental ideas:

The business was selling far below our estimate of intrinsic value.

The risks that created the value opportunity were well-known (priced-in), transitional in nature, and non-fatal.

The market seemed to be ignoring interest rate optionality which would’ve significantly changed the P&L of the company.

We were very fortunate in that our #3 played out in quick fashion as inflation in Brazil continued its decent throughout our holding period. This allowed our #2 to be priced in accordingly and ultimately addressed our #1, bridging the gap between an extreme undervaluation to a more rational price, which brings us to our reason for selling the stock.

Material Changes to the Risk/Reward Opportunity

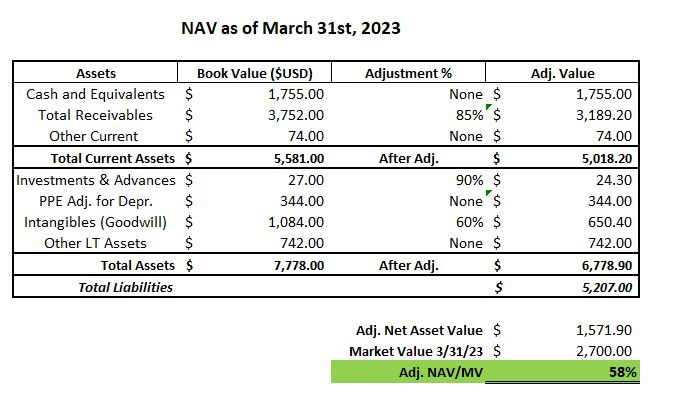

Our first step in valuing any business is to begin with the Net Asset Value (NAV). We start with this approach as it provides the most conservative estimate of what the business is worth in its current state, ignoring any forecast about the future earnings stream. We begin with the balance sheet and examine the stated asset values at the end of the most recent operating period. We know that the stated accounting values are going to be more accurate for some assets compared to others. (i.e. current tangible assets like Cash vs. long-term intangibles like Goodwill) As such, we adjust stated values based on our opinion of their reliability. When we first published our thesis for StoneCo, our NAV Model was as follows:

Based on our model, we saw that the company was trading under its stated NAV of USD $2,571B. After adjusting for accounting reliability, we still had ~60% of the market cap protected on the downside by net asset values, of which the majority being held in tangible current assets. With relatively little value given to the earnings power, what we expected to find was a struggling business with bad economics and weak prospects. Instead, we found a business that grew sales 26% from the previous year with a gross profit margin of 70%, an operating margin of ~45%, and free cash flow to be reinvested as the company saw fit. Furthermore, Brazil’s POS terminal market was expected to grow at a CAGR of 17.8% through 2028, with highly favorable trends in smartphone penetration, digital payments, and e-commerce. These combined characteristics did not make for a bad business.

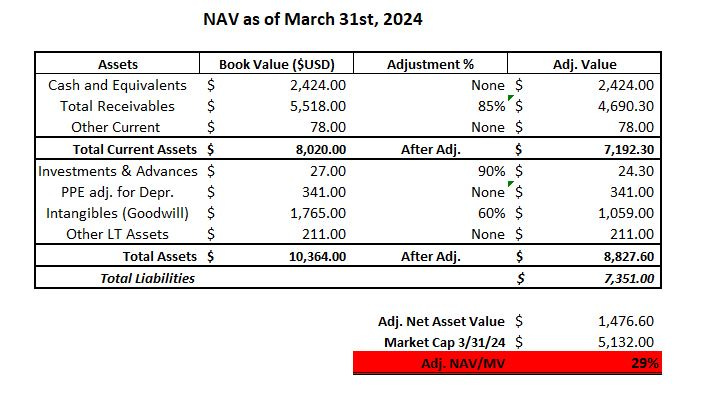

So what changed in a year?

What changed was our adjusted NAV dropped slightly to USD $ 1,476B but the market cap nearly doubled, changing the original risk/reward profile of the investment. At the higher valuation, our exposure to downside risk increased from 40% to nearly 70% from a NAV perspective. It’s important to remember that investments are not just valued in absolute terms but also relative to other opportunity sets. For us to invest in a fintech business (ever-changing industry dynamics) domiciled in Brazil (less familiar political, socioeconomic, and regulatory framework), we require a larger margin of safety than would be required for a business in a more stable industry with lower external risk factors.

From an operating perspective, Stone’s latest results also gave us some cause for concern. For example, selling expenses increased 36% year over year, while consolidated revenue grew just 14% over the same time-period. The management and board of directors have gone through numerous changes, most notably at the CEO and CFO levels since our initial investment. The latest quarter also saw Stone make an internal accounting change to revenue recognition for membership fees. The revenue is now being deferred throughout the lifetime of the client. When asked about this change on the latest earnings call, management told investors that they do not disclose how many months are currently being used to calculate customer lifetime value.

While this might be considered a minute detail in analyzing an entire business, we do care about how management communicates with investors, the simpler and more straightforward, the better. Any attempts to obfuscate data through accounting practices or language raises red flags for us. For example, a manager that must increase marketing spend due to higher competition might tell analysts they are “investing in their brand” as a euphemism. This is not to say anything illegal or fraudulent is happening at StoneCo, only that matters of risk/reward can change through qualitative as well as quantitative factors.

We hope that this discussion has given you insight into our decision to sell StoneCo at current levels. The stock may well be undervalued and continue to increase from this level. We do not make stock price predictions. However, our decisions are guided by conservative investing principles which we believe to be the cornerstone of good investing.

Thank you for reading.

Until next time,

Jack Beiro, MBA

JB Global Capital

The information contained herein represents the author’s opinion and is for informational purposes only. Nothing in this newsletter should be construed as legal, tax, investment, or financial advice. No opinion expressed by the author should be construed as a specific inducement to make a particular investment or follow a particular strategy. The author may hold positions in securities mentioned in the newsletter and may buy or sell securities at any time. The author may express opinions based on information he considers reliable, but no guarantee or warranty is made with respect to such information’s completeness or accuracy, and the author is under no obligation to update or correct any information provided. Please consult your own financial or investment advisor before acting on any information provided herein.