StoneCo Q1 2023 Earnings Review

Includes Valuation Models (Net Assets, EPV, DCF)

Listen:

Hello Fellow Investors,

Welcome back to the JB Global Capital newsletter. Today, we are going to be reviewing Stone’s Q1 earnings results that were released just this past week. If you haven’t read our previous investment case on StoneCo or need a refresher on the business, click here!

As always, thank you for being a member of our growing community. On to the article!

Business Overview:

StoneCo (STNE ) is a Brazilian payments business that empowers small and medium sized merchants to conduct electronic commerce across in-store, online, and mobile channels. The company was founded in 2012, starting with payment processing technology and a POS terminal. The business has since expanded to provide banking and credit products, along with workflow software solutions through a series of acquisitions. The broad and growing customer base of merchants enabled the company to cross-sell its banking, credit, and software offerings due to smooth integration between products.

Q1 2023 Financial Highlights - Figures converted to USD 0.00%↑

Revenue: $543.36M (+31.0% y/y)

Adj. EBITDA: $250.28M (+55.7% y/y)

Adj. EBITDA Margin: 46.3%

Free Cash Flow: $150.40M

Free Cash Flow Margin: 27.68%

StoneCo reported first quarter 2023 results on May 17th, surpassing analyst’s expectations for top and bottom line. Stone reported total revenue of $543M for the quarter, an increase of 31% compared to the same quarter last year. The growth in revenue is notable as it nearly tripled the overall industry growth at 10.7%, indicating strong market share gains for Stone. The company also saw a remarkable growth in its profitability, with adjusted earnings rising by 55.7% to $250.28M. There are not many businesses that can grow revenues above 30% a year while maintaining EBITDA margins above 40% (if you know of any, please let us know).

Stone’s Q1 results highlighted their success in taking market share from competitors, especially in the micro-merchant segment. Stone attributed the growth in the micro-merchant segment to a combination of their newly launched banking product, Super Contra Ton, and successful marketing campaigns through Brazil's most popular reality show, Big Brother Brazil. During the earnings call, management addressed these market share gains stating,

“We have a pretty granular view of who we're taking market share from, in which client tiers, in which regions… But the message is we take market share from all competitors. And the growth in TPV trends that we see is driven by our growth in the micro segments.” – Lia Matos, COO

While they did not name any competitor directly, we believe that they are largely referring to PagSeguro, another popular fintech in Brazil focused on micro-merchants.

The company, in another major development, resumed its credit business. As credit proved to be a major issue for Stone in 2021, the company has chosen to take a cautious approach, disbursing roughly $1.2M of the new credit product in the first quarter with a target of serving a maximum of only 200 clients. To improve the credit product, management has introduced several new features which include system automation, guarantees, tech-enabled decision models, and an improved credit lifecycle monitoring system. The results thus far have been positive, with key credit performance indicators in line with management expectations. During the call, management told analysts that they expect to continue expanding the credit business throughout the rest of this year.

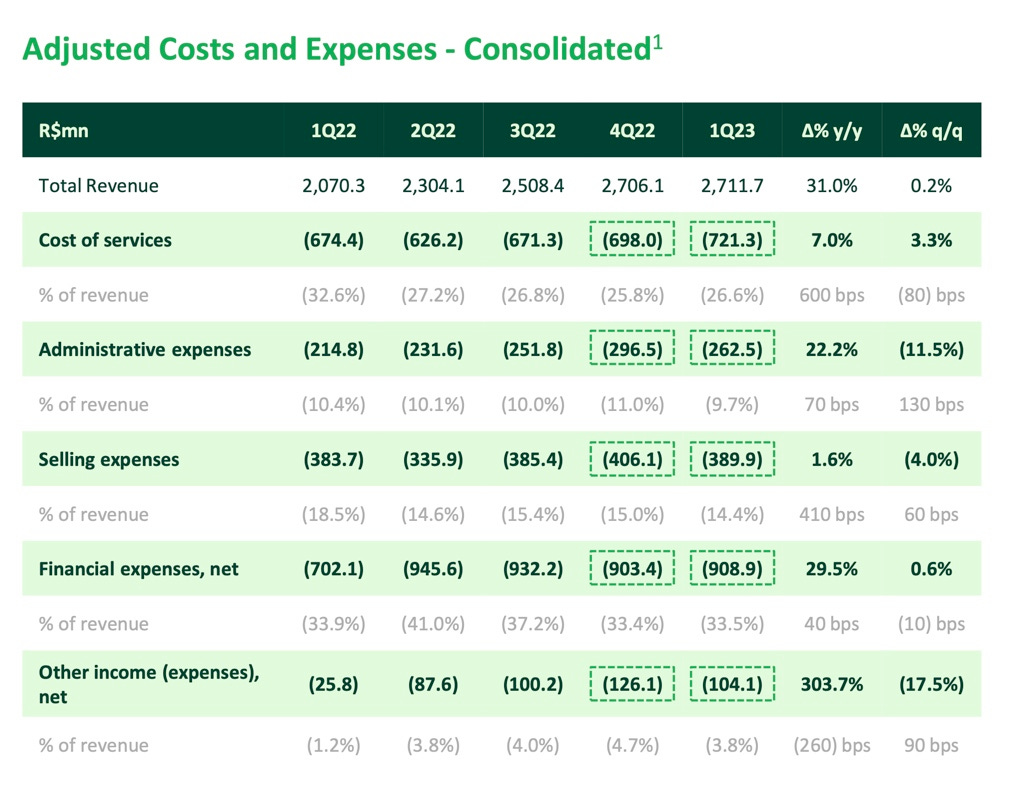

As a financial services business, StoneCo is heavily impacted by interest rates through their funding costs. Stone’s financial expenses increased 30.4% to $181M. This increase was due to a rise in interest rates in Brazil, over the comparable periods. The Selic rate currently sits at 13.75% and has been a heated topic of debate between Brazils president, Lula da Silva, and the Central Bank of Brazil. When asked during the call, how a decrease in interest rates would affect Stones business, management answered that it would result in lower funding costs, increasing Stones profitability as financial costs are currently the largest expense on the income statement. With Brazils inflation falling to its lowest level in over two years, we find it plausible that rates will be cut within the next 6-12 months, providing a significant tailwind to Stones business.

The market appears to be catching on to Stone’s undervaluation as the stock has risen 63% Year-To-Date. The Q1 results were followed by analyst upgrades and newly issued price targets which show significant upside potential for the shares. For example, Citigroup, Evercore, and Susquehanna increased their price targets on the stock to $17, $19, and $20, respectively. After reviewing the latest earnings report, we have decided to update our valuation models; starting with Net Assets, followed by an EPV model, and finally, a traditional DCF model. (See below for valuation models) In summary,

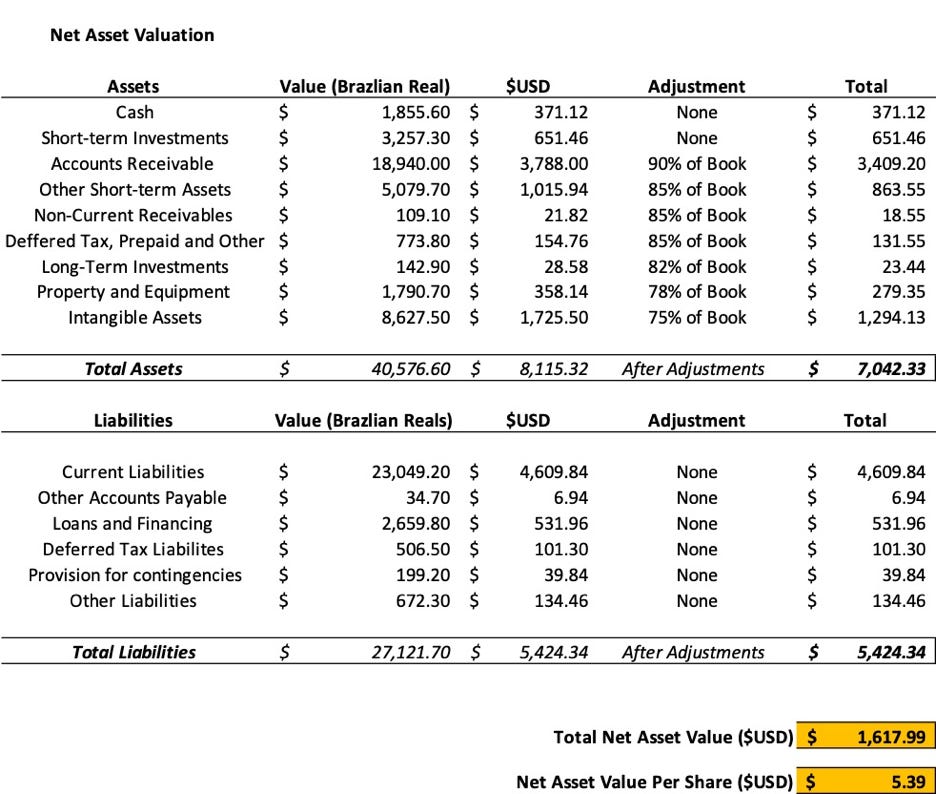

Stone’s Net Assets = $1,618B or $5.39 per share. We use this net asset value as a floor valuation for the business, and to analyze the strength of the company’s balance sheet. We also know that some accounting values are more reliable than others. Thus, as we work our way down the balance sheet, we accept or adjust the stated numbers.

Stone’s EPV Valuation= $4,919B or $16.34 per share. Earnings Power Value (EPV) is a technique for valuing stocks by assuming the sustainability of current earnings and cost of capital, but assuming no further growth. We use EPV as a conservative valuation method for analyzing what a business is worth in its current state. While it is unrealistic to believe that Stone’s profits will remain stagnant going into the future, we use the below figures as a yardstick to measure the viability of an investment at current earnings.

Stone’s DCF Valuation= $6,724B or $22.34 per share. This valuation assumes decelerating revenue growth over the next 10 years and a WACC of 18.45% to account for country and currency risk. This indicates that at current prices, Stone is undervalued by ~62%.

If you enjoy our content, make sure to subscribe for more!

Valuation #1: Net Asset Value

Valuation #2: Earnings Power Value

Valuation #3: DCF Results

Thank you for reading todays article! We hope you found it valuable. If you have, please make sure to leave a like or comment below.

Until next time!

Sincerely,

Jack Beiro, MBA

JB Global Capital

STNE 0.00%↑ PAGS 0.00%↑ NU 0.00%↑

The information contained herein represents the author’s opinion and is for informational purposes only. Nothing in this newsletter should be construed as legal, tax, investment, or financial advice. No opinion expressed by the author should be construed as a specific inducement to make a particular investment or follow a particular strategy. The author may hold positions in securities mentioned in the newsletter and may buy or sell securities at any time. The author may express opinions based on information he considers reliable, but no guarantee or warranty is made with respect to such information’s completeness or accuracy, and the author is under no obligation to update or correct any information provided. Please consult your own financial or investment advisor before acting on any information provided herein.

Excellent read! Would love to see more earnings report articles!