StoneCo (STNE) Q3 2023 Earnings Review

Improvements All Around

Audio:

Business Overview:

StoneCo Ltd is a provider of financial technology solutions. The company offers solutions that empower merchants to conduct electronic commerce seamlessly across in-store, online, and mobile channels in Brazil. The company was founded in 2012 as a merchant acquirer, but has since expanded into software and lending, similar to its U.S. peer, Block. The company has financial backing from major global players such as Warren Buffet’s Berkshire Hathaway, Cathie Wood’s Ark Invest, and Jack Ma’s Ant Group. The company will have its Investor Day on November 15th, where management plans to share their views on the business and their long-term strategic plans.

Q3 Financial Highlights (Figures converted from R$ to USD$):

Revenue: $628M (+25% y/y)

Earnings Before Taxes: $101M (+20% y/y)

EBT Margin: 16%

Net Income: $82M

NI Margin: 13%

Brazilian financial tech firm StoneCo reported impressive Q3 results on Friday, leading to a ~5% gain on the stock after-hours. The company saw its adjusted net profit in the third quarter more than quadruple, landing above analysts' estimates off the back of solid growth in its financial services segment. The firm reported revenue of $628 million, in line with estimates and up 25.2% year-on-year, boosted by a 29% increase in revenues from its financial services segment. Earnings before taxes (EBT) came in at roughly $100M, growing 20% from the previous year. Stone's total payments processed (TPV) in the quarter totaled $17.92 billion, up 20% from a year earlier and above the firm's top-end projections. It’s take-rate for the segment stood at 2.49% in the three months ended in September, growing both YoY and sequentially.

The company continues its ascent in the Brazilian payments space, growing more than double the overall industry. This growth signals that Stone is successfully taking market share away from competitors in the MSMB segment. While the operating results for the quarter were impressive, we were equally impressed by the company’s capital allocation strategy. The company announced a $60 million repurchase program on September 21st, 2023. On the call, management confirmed that they have already concluded the repurchase of the whole program in November. We believe that Stone should continue to repurchase shares, given the low share-price relative to the long-term cash generation capabilities of the company. Speaking directly to Stone’s capital allocation decisions, CFO Mateus Scherer stated,

“When you look at the third-quarter results, we can see that the company is generating strong cash flows. As our business evolves, we do expect our profitability to continue to increase, and this should drive even more cash generation. We still see a lot of room to reinvest in the business in general. But whenever we feel there is a good opportunity to allocate excess cash, for example, toward repurchases, we're certainly going to evaluate this option.”

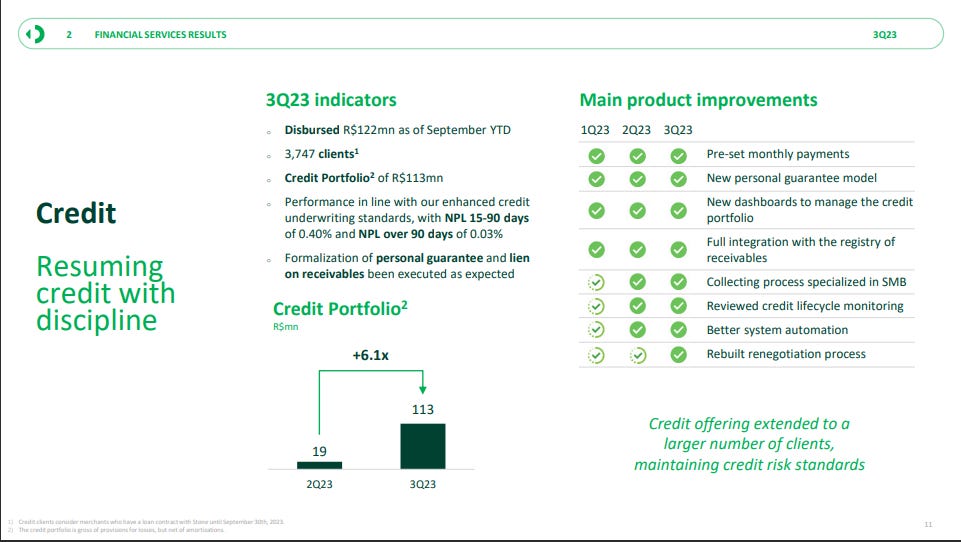

On another positive note, the company has significantly accelerated its credit operation, with the portfolio growing over 6X sequentially. As the credit business begins to contribute more to Stone’s bottom line, we see the firms shares going through a dramatic re-rating in the near future. In other words, If Stone can successfully grow their credit business to pre-pandemic levels, we believe that the shares are considerably undervalued at the time of writing.

Hello Reader! If you are enjoying the content, we highly recommend subscribing for more!

Updated Valuation:

Stone’s Net Asset Valuation = $1.5B or $4.90 per share. We use this net asset value as a floor liquidation value for the business, and to analyze the strength of the company’s balance sheet. As some accounting values are more reliable than others, we accept or adjust the stated numbers on the financial statements. This process leads to an ultra-conservative estimate of Stone’s stated net-asset value.

Stone’s EPV Valuation= $3.1B or $10.25 per share. Earnings Power Value is a technique for valuing stocks by assuming the sustainability of current earnings and cost of capital, but assuming no future growth. We use EPV as a conservative valuation method for analyzing what a business is worth in its current state.

Stone’s DCF Valuation= $5.5B or $17.86 per share. This valuation assumes decelerating revenue growth over the next 10 years and a WACC of 24.15% to account for country and currency risk. At the time of writing, Stone is currently valued at $10.72 per share. This would indicate that the company is significantly undervalued. We look forward to Investor Day on the 15th and will recap our thoughts on the event within the next couple of weeks.

Thanks for reading! We hope you enjoyed the analysis. All feedback is appreciated in the comments below.

Sincerely,

Jack Beiro, MBA

JB Global Capital

The information contained herein represents the author’s opinion and is for informational purposes only. Nothing in this newsletter should be construed as legal, tax, investment, or financial advice. No opinion expressed by the author should be construed as a specific inducement to make a particular investment or follow a particular strategy. The author may hold positions in securities mentioned in the newsletter and may buy or sell securities at any time. The author may express opinions based on information he considers reliable, but no guarantee or warranty is made with respect to such information’s completeness or accuracy, and the author is under no obligation to update or correct any information provided. Please consult your own financial or investment advisor before acting on any information provided herein.

I always enjoy your research and loved this post in particular. I hold a (6%) position in stne for similiar reasons.

One thing I often find strange is the usage of wacc and country risk in evaluating businesses.

a) the important factor for value creation is the cost of capital (in relation to the return on capital amd reinvestment rate). It doesn't matter for e.x. that the default rate in a country is high (too much leverage used by other companies) if you invest in a profitable company with ample net cash. It doesn't make the cost of capital greater or the returns of investing in the company smaller

b) In general I find the usage of wacc peculiar. It makes sense to compare the return on capital of projects/businesses to the average cost of capital to understand if the project makes sense. However when buying another company we should compare their return on capital to our cost of capital as we are the ones investing the capital

In my (humble) opinion it makes more sense to use the same discount rate for all companies (our wacc - but it can be any number really as long as we are consistent, I use 10) and just demand more margin of safety for riskier securities.